Student loans are forms of financial assistance used to help students access higher education. Student lending debts in the United States have grown tremendously since 2006, rising to nearly $ 1.4 trillion by the end of 2016, about 7.5% of GDP. Approximately 43 million have student loans, with an average balance of $ 30,000. In 2017, the average student loan debt reached $ 39,400, an increase of 6% compared to 2016. Americans owe more than $ 1.48 trillion (44 million borrowers) which is approximately $ 620 billion more than the entire debt credit card in that country. Loans usually have to be repaid, in contrast to other forms of financial assistance such as scholarships, which are never to be repaid, and grants, which are rarely to be repaid. Research shows an increased use of student loans has been a significant factor in increasing tuition fees.

Video Student loans in the United States

Overview

Student loans play a huge role in US higher education. Nearly 20 million Americans attend classes each year. Of that amount, 20 million, almost 12 million - or 60% - borrow each year to cover costs. In Europe, higher education receives more funds from the government, so student loans are much more common. In parts of Asia and Latin America government funding for lower post-secondary education - usually limited to some top universities, such as UNAM Mexico - and no special programs where students can easily and inexpensively borrow money. However, in the United States, many colleges are funded by students and their families through loans, although public institutions are funded in part through state and local taxes, and both private and public institutions through Pell grants and, especially with older schools, donors and alumni, and investment income. Some believe this substantially increases the intergenerational correlation in income (having two generations of families having the same earning ability), although other factors, including genetics, have been estimated to play a larger combined role. Nonetheless, higher education in the United States has proven to be an excellent investment both for individuals and for the public, although the difference in returns on education investment in schools has been exaggerated in many cases.

Student loans come in several varieties in the United States, but are basically divided into federal loans and private student loans. The federal loan, which FAFSA is the application, is divided into subsidized (the government pays interest when students learn at least half the time) and is not subsidized. Federal student loans are subsidized at the undergraduate level only. Subsidized loans are by far the best type of loan, but unsubsidized federal student loans are much better than private student loans. Some states have their own lending programs, as do some universities. In almost all cases, these student loans have better conditions - sometimes much better - than the highly advertised and expensive private student loans.

Student loans can be used for college-related fees, including school fees, rooms and meals, books, computers, and transportation costs.

Unusual rules in the law prohibit student loans issued through bankruptcy.

The main types of student loans in the United States are as follows:

- Federal student loans are made to students directly (Stafford and Perkins loans). This loan is made regardless of credit history (most students have no credit history); automatic approval if students meet the program requirements. Students do not make payments when enrolling in at least part-time studies. If a student drops below half the time or graduate, there is a six-month grace period. If a student re-enrolls at least half the time of the status, the loan is suspended, but when they fall below half the time they no longer have access to the grace period and payment should begin. All Perkins loans and some Stafford undergraduate loans receive subsidies from the federal government. Unsubsidized and unsubsidized subsidized loans are limited.

- There is a lot of delay and some patience (loan cancellation) that can be found in the Direct Loan program. For those who are disabled, there is also the possibility of 100% loan discharge (loan cancellation). Due to changes by the 2008 Higher Education Opportunity Act, it becomes easier to get one of these releases after July 1, 2010. There is a provision of loan forgiveness for teachers in certain critical subjects or in schools with more than 30% of students at meal prices reduced lunch (the general measure of poverty), and qualify for loan forgiveness from all of their Federal Family Education Program Stafford, Perkins and Loan Program loans up to $ 77,500. In addition, any person employed full-time (in any position) by a 501 (c) (3) non-profit, or other eligible public service organization, or serving in a full-time AmeriCorps or Peace Corps position, qualifies for lending forgiveness (cancellation) after 120 qualifying payments. 120 monthly payments of qualification need not be consecutive; they may be subject to impunity if there is a term of employment with an unqualified employer. However, the pardon or disposal of the loan is considered as taxable income by the Internal Revenue Service under 26 U.S.C. 108 (f).

- A federal student loan granted to a parent (PLUS loan): A much higher limit, but payments begin immediately. Credit history considered; approval is not automatic.

- Private student loans, made for students or parents: Higher limits and no payment until after graduation, although interest starts to accrue immediately and the deferred interest is added to the principal, so there is interest in interest (deferred) ( which is not the case with subsidized student loans). Interest rates are higher than federal loans, set by the United States Congress. Private loans are, or should be, the last option, when federal and other loan programs are exhausted. Any college financial support officer will recommend you to borrow a maximum under a federal program before switching to a personal loan.

Maps Student loans in the United States

Federal loan

Federal federal loans to students

US government-backed student loans were first offered in 1958 under the National Defense Education Act (NDEA), and are only available for selecting student categories, such as those studying in engineering, science, or educational degrees. The student loan program, along with other sections of the Act, which subsidize the training of university professors, was established in response to the launch of Sputnik satellites by the Soviet Union, and the widespread perception that the United States lags behind in science and technology, amidst the Cold War. Student loans extended more widely in 1960 under the Higher Education Act of 1965, with the aim of encouraging greater social mobility and equal opportunity.

Prior to 2010, Federal loans include direct loans - originated and funded directly by the US Department of Education - and secured loans - originated and funded by private investors, but guaranteed by the federal government. The secured loans were abolished in 2010 through the Student Assistance and Fiscal Responsibility Act and were replaced by direct loans due to the belief that secured loans benefit private lending companies with taxpayer fees, but do not reduce costs for students.

These loans are available to students and college students through funds channeled directly to schools and are used to supplement personal and family resources, scholarships, grants, and work studies. They may be subsidized by the US Government or may not be subsidized depending on financial needs. The US Department of Education publishes a booklet that compares federal loans with personal loans. In this same document, the government explains what you can use the loan to:

You can use the money you receive just to pay for tuition fees at the school that gives you the loan. Tuition fees include school fees such as tuition; room and dining; cost; book; stock; equipment; dependent childcare costs; transport; and leasing or purchasing a personal computer.

Subsidized and unsubsidized loans are guaranteed by the US Department of Education either directly or through a guarantee agency. Loans granted are Stafford and Perkins loans arranged by the US Department of Education. Almost all students are eligible to receive federal loans (regardless of credit score or other financial issues). Federal student loans are not priced according to the size of individual risk, as well as the loan limit is determined by risk. On the contrary, pricing and borrowing limits are politically determined by Congress. Undergraduate students usually receive lower interest rates, but graduate students can usually borrow more. This lack of risk-based pricing has been criticized by scholars as contributing to inefficiencies in higher education.

Both types offer a six-month grace period, which means that no payments are due up to six months after graduation or after the borrower becomes less than half a student without graduation. Both types have fairly simple annual limits. The effective dependent bachelor limits for loans disbursed on or after July 1, 2008 are as follows (combined subsidies and non-subsidized restrictions): $ 5,500 per year for new undergraduate students, $ 6,500 for undergraduate students, and $ 7,500 per year for students junior and senior scholars, as well as students enrolled in teacher certification or preparatory courses for graduate programs. For independent students, the limit (subsidized and unsubsidized combination) effective for loans disbursed on or after July 1, 2008 is higher: $ 9,500 per year for new undergraduate students, $ 10,500 for undergraduate students, and $ 12,500 per year for undergraduate students junior and senior, as well as students enrolled in teacher certification or preparatory courses for graduate programs. Subsidized federal student subsidies are only offered to students with indicated financial needs. Financial needs may vary from school to school. For this loan, the federal government makes interest payments when the student is in college. For example, those who borrow $ 10,000 during college owe $ 10,000 after graduation.

Unsubsidized federal student loans are also guaranteed by the US Government, but the government, while controlling interest rates, does not pay interest to students, not interest earned during college. Almost all students qualify for this loan regardless of financial needs (based on need, see Expected Family Contributions). Those who borrow $ 10,000 during college owe $ 10,000 plus interest upon graduation. For example, those who borrow $ 10,000 and earn $ 2,000 in interest rates owe $ 12,000. Interest begins at $ 12,000, that is, there is interest in interest. The accrued interest is "capitalized" into the loan amount, and the borrower starts making payments on the total accumulation. Students can pay interest while still in college, but few do.

Federal student loans to graduate students have higher limits: $ 8,500 for Stafford subsidized and $ 12,500 (limit may be different for certain courses) for Unsubsidized Stafford. Many students also avail Federal Perkins Loans. For graduate students, the limit for Perkins is $ 6,000 per year.

Limit aggregate loan Stafford

Students who borrow money for education through Stafford loans can not exceed certain aggregate limits for subsidized and unsubsidized loans. For undergraduate-dependent students, the combined maximum limit of subsidized loans and unbundled subsidized loans is $ 57,500, with subsidized loans limited to a maximum of $ 23,000 of total loans. Students who have borrowed the maximum amount in subsidized loans can be (based on grade level - graduate, postgraduate/professional, etc.) Taking loans of less than or equal to the amount they will qualify for subsidized loans. Once the subsidized and unsubsidized aggregate boundaries have been met for subsidized and unsubsidized loans, students can not borrow additional Stafford loans until they repay part of the loan. A student who has repaid part of this amount regains eligibility to the aggregate limit as before.

The graduate student has a lifetime loan limit of $ 138,500.

Federal student loans to parents

Usually this is a PLUS loan (previously standing for "Parent Loans for Undergraduate Students"). Unlike loans given to students, parents can borrow more, usually enough to cover the remaining costs that are unattainable by the student's financial aid. Interest increases during student time in school. Interest rates for PLUS loans per 2017 are 7% for Stafford loans. No payment is required until the student is no longer in school, although parents can start paying in advance if they wish, thus saving interest.

Parents are responsible for the repayment of these loans, not students. Loans to parents are not 'kosigner' loans with students having equal accountability. The parents have signed the main promissory notes to repay the loan and, if they do not return the loan, their credit rating will suffer. In addition, parents are advised to consider what their monthly payments are after borrowing for four years at this rate (early loan documents will provide repayment schedules as if only one year loan is taken). What sounds like a "controllable" debt burden (for example) $ 200 a month from a first year loan can creep into a frightening 800 US dollars per month by the time four years have been funded through loans. Borrowing is not free, and the more loans, the more expensive.

Under the new law, postgraduate students are entitled to receive PLUS loans on their own behalf. This Graduate PLUS Loan has the same interest rate and the terms of the Parent PLUS loan.

The current interest rate on this loan is 7%.

Disbursement: How money gets to students or schools

Federal Direct Student Loans, also known as Direct Loans or FDLP loans, are funded from public capital originating from the US Treasury. FDLP loans are distributed through channels starting with the US Treasury Department and from there through the US Department of Education, then to college or university and then to students.

According to the US Department of Education, over 6,000 colleges, universities and technical schools participate in FFELP, which represents about 80% of all schools. FFELP loans represent 75% of all federal student loans.

In 2010, the Healthcare Reform Act included provisions on Education, which ended the Federal Family Education Loan Allocation after 30 June 2010. From that date, all government-backed student loans have been issued through the Direct Loan program.

Debt level

The maximum amount each student can borrow is subject to federal policy changes. The current loan limit is below the costs of most four-year private institutions and most major public universities, and therefore students typically borrow high-cost private student loans to make a difference. Scholars have advocated increasing the federal debt limit to reduce interest costs to student debtors.

The maximum amount each student can borrow is subject to federal policy changes. A study published in the 1996 winter edition of the Student Financial Support Journal , "How Much Loans Are Student Loans Too Much?" suggest that the payment of student debt on a monthly basis for an undergraduate average may not exceed 8% of total monthly income after graduation. Some financial aid advisors refer to this as an "8% rule." Circumstances vary for individuals, so the 8% level is an indicator, not a rule set in stone. A research report on the 8% level is available at the Iowa College Student Aid Commission. Of the 100 students who had attended a nonprofit organization, 23 failed in 12 years after starting college in the 1996 group compared to 43 in the 2004 group (compared with an increase of only 8 to 11 students among participants who had never attended the for-profit training).

The Economist reported in June 2014 that the debt of US student loans exceeded $ 1.2 trillion, with more than 7 million debtors in default. Debt and negligence among black students is at a crisis level, and even undergraduate degrees do not guarantee safety: black BA graduates fail on five white BA graduates (21 to 4 percent), and are more likely to fail than white breaks. Public universities increase their costs by a total of 27% over the five years ending in 2012, or 20% adjusted for inflation. General university students pay an average of nearly $ 8,400 per year for tuition fees in the state, with students outside the country paying more than $ 19,000. Over the two decades that ended in 2013, tuition has risen 1.6% more than inflation every year. Government funding per student fell 27% between 2007 and 2012. Admissions increased from 15.2 million in 1999 to 20.4 million in 2011, but down 2% in 2012.

Standard payment

When a Federal student loan enters a payment, they are automatically registered in the default payment . Below, a borrower has 10 years to repay the total amount of the loan. The loan provider (whoever sends the bill) determines the monthly bill by calculating the fixed monthly payment amount which will pay off the initial loan amount plus all accrued interest after 120 equal payments (12 payments per year).

Payment pays interest incurred each month, plus a portion of the original loan amount. Depending on the loan amount, the loan term may be shorter than 10 years. There is a minimum monthly payment of $ 50.

Income Based Revenue Plan

If student loan debt is high but their income is simple or zero, they may be eligible for an income-based payment plan (IDR). Most types of federal student loans - except PLUS loans for parents - are eligible for the IDR plan. The revenue-driven package allows borrowers to limit their monthly payments to 10%, 15%, or 20% of disposable income up to 20 or 25 years, after the remaining balance is forgiven.

Currently, four custom IDR is available:

1. Income Based Income (IBR)

2. Pay As You Get (PAYE)

3. Revise Pay As You Get (REPAYE)

4. Payment of Contingencies (ICR)

Student loan expenditure

US federal student loans and some private student loans may be exhausted in bankruptcy simply by showing "undue difficulties." Unlike credit card debt, which can often be disposed of through bankruptcy proceedings, this option is generally not available for educational loans. In addition, those who seek to pay off their student loan debt should start a hostile process, a separate lawsuit in case of bankruptcy in which they describe the difficulties required. Many borrowers can not afford to keep lawyers or additional litigation fees associated with the trial process, let alone bankruptcy cases. A more complicated issue, undue standards of difficulty vary from jurisdiction to jurisdiction, but generally difficult to fulfill, making student loans practically indestructible through bankruptcy. In most circuit discharges depends on meeting the three branches in the Brunner test:

As noted by the district court, there is little authority to appeal on the definition of "undue difficulties" in the context of 11 U.S.C. Ã, § 523 (a) (8) (B). Based on the legislative history and the decision of the district court and other bankruptcies, the district court adopted the standard for "undue difficulties" which requires three parts which indicate: (1) that the debtor can not maintain, based on current income and expenditure, "minimal" standard of living for himself and his dependents if forced to repay the loan; (2) that there are additional circumstances which indicate that this situation is likely to persist for most of the student repayment period; and (3) that the debtor has made a good faith effort to repay the loan. For the reasons set forth in the district court order, we adopt this analysis. The first part of this test has often been applied as the minimum required to build "undue difficulties." See, for example, Bryant v. Pennsylvania Higher Educ. Relief Society (In re Bryant), 72 B.R. 913, 915 (Bankr.E.D.Pa.1987); North Dakota State Bd. from Higher Educ. v. Frech (In re Frech), 62 B.R. 235 (Bankr.D.Minn.1986); Marion v. Pennsylvania Higher Educ. Assistance Agency (In re Marion), 61 B.R. 815 (Bankr.W.D.Pa.1986). Needing a show like that suits common sense as well.

While federal student loans can be administratively dismissed for total and permanent disability, private student loans can not be disposed of outside bankruptcy.

A set of empirical data comes from the Education Credit Management Corporation, which serves loans to twenty-five loan agencies and the US Department of Education; in 2008 it was reported that of 72,000 loans in bankruptcy proceedings, only 276 debtors were repealed, and in November 2009 out of 134 resolutions so far, 29 resulted in total or partial disengagement.

A review of records in the United States Bankruptcy Court for the Western District of Washington found that 57% of the 115 court proceedings reviewed in the 5 year period resulted in partial relinquishment, through settlement or trial; However, the authors warn not to generalize the results of this small sample. 86% are involved either (or both) the United States Department of Education or Education Credit Management Corporation, a nonprofit institution that provides loans where students have declared bankruptcy.

The rules for the release of total and permanent disabilities underwent major changes as a result of the 2008 Higher Education Opportunity Act. Loan holders are no longer required to be unable to earn any income, but instead the standard is a "very profitable activity" (SGA) as due to disability. The new regulation takes effect from 1 July 2010. Under further changes as of July 1, 2013, if the borrower is determined to be disabled by the Social Security Administration, that resolve will be accepted as total and permanently disabled if SSA places individuals in the five- year (the longest currently used by SSA). Effective with disposal on or after January 1, 2018, debt disposed of by death or total permanent disability from the borrower is no longer treated as taxable income. This provision, part of the Tax Cut and the Employment Act of 2017, will expire on 31 December 2025 unless renewed by the Congress.

Private student loans

These are loans that are not guaranteed by government agencies and made for students by banks or financial companies. Private loans are more expensive and have far less favorable terms than federal loans, and are generally only used when students have spent borrowing limits under federal student loans. They are not eligible for an Income Based Return plan, and often have less flexible payment terms, higher fees, and more fines.

Private student loan advocates suggest that they combine the best elements of different government loans into one: they generally offer higher borrowing limits than federal student loans, ensuring students are not left behind by the budget gap. Unlike federal parent loans (PLUS), they generally offer a six-month grace period (sometimes 12 months) without payment until after graduation; however, interest is increased and added to the principal. Most experts unrelated to the private lending industry recommend private student loans only as an expensive last resort, because of higher interest rates, double fees, and the lack of borrower protection built into federal loans.

Type of private student loan

Private student loans generally come in two types: school-channel and direct to the consumer.

School channel loans offer lower interest rate borrowers but generally take longer to process. School channel loans are "certified" by the school, which means the school is withdrawing from the loan amount, and the funds are disbursed directly to the school. "Certification" simply means that the school insists that the loan fund will be used only for educational expenses, and agrees to hold it and disburse it as needed. Certification does not mean that the school approves, recommends, or even checks the terms (conditions) of the loan.

Direct personal loans to consumers are not certified by the school; schools do not interact with personal loans directly to consumers at all. Students only verify registration to the lender, and the proceeds are distributed directly to the student. While direct loans to consumers generally carry higher interest rates than school channel loans, they allow families to get access to funds very quickly - in some cases, on a daily basis. Some argue that this convenience is offset by the risks of overly borrowed students and/or the use of funds for inappropriate purposes, since no third-party certification of loans is appropriate for the educational needs of the students concerned. , or that it will only be used for education.

Direct personal loans to consumers are the fastest-growing segment of educational financing with "the percentage of students who get private loans from 2003-04 to 2007-08 goes from 5 percent to 14 percent" and is under legislative oversight due to lack of school certification. Loan providers range from large educational finance companies to specialized companies that focus exclusively on these niches. Lenders often encourage such loans with advertising: "no FAFSA is required," or "Funds are channeled directly to you." But since the passing of the Health and Education Reconciliation Act of 2010 (HCERA), the death knell was heard for private sector loans under the Federal Family Education Loan Program (FFELP). Since July 1, 2010, no new student loans are made under FFELP; all subsidized and unsubsidized Stafford loans, PLUS loans, and Consolidation loans have been made entirely under the Federal Direct Loan Program.

Interest rate of private student loan and interest

Federal student loan interest rates are set by Congress, and are set. Private student loans usually have much higher interest rates, and prices fluctuate depending on the financial markets. Some private loans disguise actual borrowing costs by requiring a large initial "cost", which allows low interest rates to be offered. Interest rates also vary depending on the credit history of the applicant.

Most private lending programs are linked to one or more financial indexes, such as the Wall Street Journal Prime rate or BBA LIBOR rate, plus additional fees. Since personal loans are based on the credit history of the applicant, the overhead costs vary. Students and families with excellent credit generally receive lower interest rates and smaller loan origination costs than those with a poorer credit history. Money paid for interest is now tax deductible. However, lenders rarely provide full details about the requirements of private student loans until after the student submits an application, in part because it helps prevent comparison based on cost. For example, many lenders only advertise the lowest interest rate they charge (for good credit borrowers). Borrowers with bad loans can expect an interest rate of 6% higher, a 9% higher borrowing fee, and a two-thirds loan limit lower than the advertised rate.

Private student loan fees

Personal loans often carry origination fees, which can be very large. The origination fee is a one-time fee based on the loan amount. They can be taken from the total amount of the loan or added above the total amount of the loan, often on the borrower's preference. Some lenders offer low-interest loans and 0 fees. Each percentage point on a front-end fee is paid once, while each percentage point on the interest rate is calculated and paid over the life of the loan. Some people suggest that this makes the interest rate more important than the origination fee. The amount borrowed from private lenders accumulates to about 15 billion loans from personal loans.

In fact, there is an easy solution to the fee-vs.-rate question: All lenders are legally required to give you an "APR (Annual Percentage Rate)" statement for the loan before you sign the promissory note and commit to me t. Unlike the "basic" tariff, this rate includes fees charged and can be considered an "effective" interest rate including actual interest, fees, etc. When comparing loans, it may be easier to compare APRs rather than "assessing" to ensure comparisons between apples and apples. APR is the best benchmark for comparing loans that have the same repayment terms; however, if the payment terms are different, the APR becomes a less than perfect comparison tool. With different term loan, consumers often see "total cost of financing" to understand their financing options.

Forwarding of private student loans

Eligible loan programs generally issue loans based on the credit history of the applicant and any applicable cosigner/co-endorser/coborrower. This is in contrast to federal loan programs that primarily address needs-based criteria, as defined by EFC and FAFSA. For many students, this is a big advantage for personal loan programs, because their families may have too many incomes or too many assets to qualify for federal assistance but insufficient assets and incomes to pay for school without help. The benefit of the joint signatories is that the lender considers the income and credit history of both students and signatories together, which increases the likelihood of students being approved for student loans.

Many international students in the United States can obtain personal loans (they are usually not eligible for federal loans) with a cosigner who is a citizen of the United States or a permanent resident. However, some graduate programs (especially top MBA programs) have ties to private lending providers and in such cases are not required cosigners even for international students.

Once students and signatories together with students are approved for student loans, private lending lenders may offer the option of co-signing release, which "releases" the joint signatories of financial responsibility for student loans. There are several student loan lenders that offer co-signatory releases and other benefits.

Personal student loan requirements

Unlike federal loans, whose requirements are public and standard, the requirements for private loans vary from lender to lender. However, it is not easy to compare it, as some conditions may not be revealed until students are presented with a promissory note to sign. The general advice is to go around on all terms, not just responding to "tariffs as low as..." tactics that are sometimes little more than bait-and-switch. However, spending around can damage your credit score. Examples of terms and benefits of other borrowers differ by lender are delays (amount of time after leaving school before payment begins) and patience (period when payment is suspended due to financial or other difficulties). These policies are solely based on contracts between the lender and the borrower and are not governed by the Ministry of Education policy.

Criticism of U.S. student loan program

In 1987, then Minister of Education William Bennett argued that "... the increase in financial aid in recent years has allowed universities and universities to brilliantly raise their dues, convinced that Federal loan subsidies will help dampen the rise." This statement came to be known as the "Bennett Hypothesis." In July 2015 (revised in March 2016), the Staff Report was published by the Federal Reserve Bank of New York, a conclusion indicating that institutions that are more exposed to an increase in student loan programs tend to respond with a disproportionate increase in college prices:

In this paper, we use a Bartik-like approach to identify the effect of increased supply of loans on tuition after major policy changes in the maximum federal assistance program available to undergraduate students occurring between 2008 and 2010. We build specific institutional changes in the maximum program as maximum institutional exposure interaction in each aid program (part of the qualified student) and the maximum program enacted. We found that the most exposed institutions with this maximum amount ahead of the policy changes incurred a disproportionate tuition hike around these changes, with effects of changes in Pell Grant's specific maximum program, subsidized loans and unsubsidized loans of around 40, 60 and 15 cents dollars, respectively.

The federal student loan program has been criticized for not adjusting interest rates according to the riskiness of factors that are under the control of students, such as the choice of academic majors. Critics argue that this lack of risk-based pricing contributes to the inefficiency and misallocation of resources in higher education, and lower productivity in the labor market. However, recent research indicates that while high student loan rates, coupled with high default rates, present a number of challenges for individual student loan borrowers and for the federal government (which must include defaults through taxes), they do not always place a great burden on the wider community.

After the passage of the bankruptcy reform bill of 2005, both federal and private student loans did not run out during bankruptcy (prior to the passage of the bill, only federal student loans can not be dismissed). It provides loan-free credit risk for lenders, averaging 7 percent per year. In January 2013, the "Fairness for Struggling Students Act" was inaugurated. This bill, if passed, will once again allow private student loans to be released in bankruptcy. The bill was referred to the Senate Judiciary Committee where he died.

Some critics of financial aid claim that, because schools believe in receiving whatever fees happen to their students, they feel free to raise their fees to a very high level, to accept students with inadequate academic ability, and to produce too many graduates in some fields of study. About a third of students, whether they graduate or find jobs that fit their credentials, are financially burdened for most of their lives with their debt obligations, rather than being economically productive citizens. When former students fail to meet their obligations, expenses are transferred to taxpayers. Finally, the proportion of graduates from poor backgrounds has actually declined since 1970.

In 2007, New York Attorney General Andrew Cuomo led an investigation into the practice of lending and anti-competitive relationships between student and university lenders. In particular, many universities are directing student borrowers to "preferred lenders" who charge higher interest rates. Some of these "preferred lenders" allegedly rewarded the university's financial support staff by kicking their backs. This has led to changes in lending policies at many major American universities. Many universities have also returned millions of dollars in return costs to affected borrowers.

The biggest lenders, Sallie Mae and Nelnet, were criticized by borrowers. They often find themselves involved in the most serious lawsuits filed in 2007. Claims False claims filed on behalf of the federal government by former Research Department researchers, Dr. Jon Oberg, against Sallie Mae, Nelnet, and others. lender. Oberg argues that lenders are burdening the United States Government and diluting taxpayers more than $ 22 million. In August 2010, Nelnet completed the lawsuit and paid $ 55 million.

In an effort to increase student loan markets, startups such as LendKey, SoFi (Social Finance, Inc.) and CommonBond were established to offer student loans and loan refinancing at lower rates than traditional payment systems using alumni-funded models. According to a 2016 analysis by the online student loan market Kredible, about 8 million borrowers can qualify to refinance their loans at lower interest rates.

The New York Times publishes an editorial in 2011 to support allowing personal loans to be re-dismissed during bankruptcy.

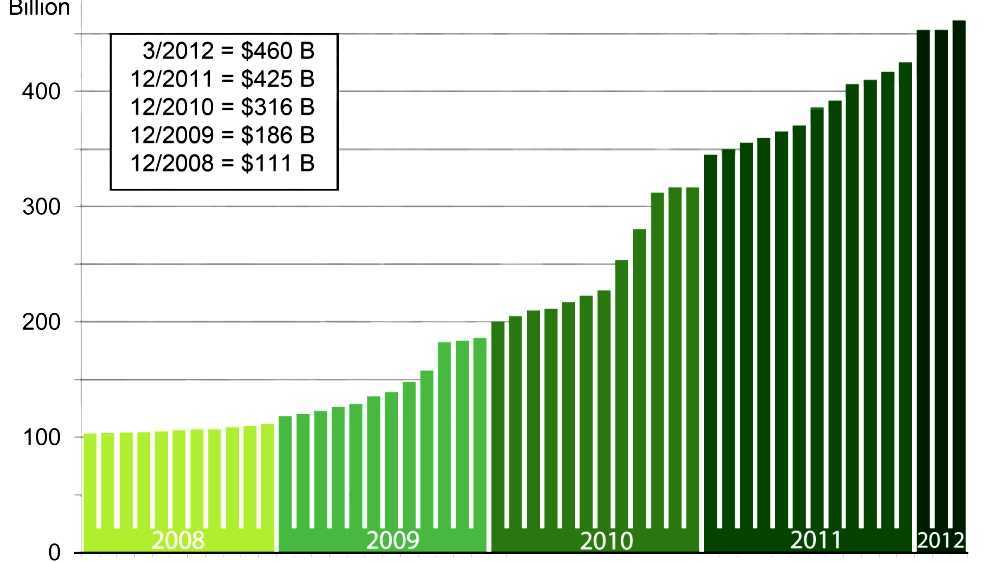

As of June 2010, the amount of student loan debt held by Americans exceeds the amount of credit card debt held by Americans. At that time, student loan debt reached at least $ 830 billion, of which about 80% is federal student loan debt and 20% is private student loan debt. In the fourth quarter of 2015, total outstanding student-owned and securities loans have increased to, and exceeded, $ 1.3 trillion. The increased student debt is contributing to the widening wealth gap.

With each passing year, student debt continues to rise. Nearly two-thirds of scholars are in debt. With graduation, their student loan debt averages around $ 26,600. One percent of graduates leave college with $ 100,000 or more student loan debt. By 2013, federal debt has grown to $ 16.7 trillion. Six percent of the debt comes directly from student loans that make student loans only second to mortgages in consumer debt. The Consumer Financial Protection Bureau reported that in May 2013, the federal student loan debt has reached $ 1 trillion so the total student debt debt amounts to $ 1.2 trillion. However, this amount does not include what students take from a savings account, a loan from a parent, or a charge to their credit card to pay for their tuition fees. In fact, the student debt burden is much larger than these figures. The Federal Reserve Bank of New York February 2017 Quarterly Report on Debt and Household Credit reports that 11.2% of aggregate student loan debt is 90 days or more in arrears in the last quarter of 2016.

Student Loans 2018

The US Congress approved a $ 350 million funding for Student Loan Forgiveness Plan as part of the $ 1.3 trillion federal government. Many financial analysts claim the program failed. The education department may remove the loan even if the student is not eligible for the Public Service Loan Forgiveness Program because it is not listed in the eligible payment plan. The Public Service Loan Forgiveness Program frees the balance in direct loans if the borrower completes 120 monthly payments under the payment plan while working full-time by an accredited employer. There is a form to be completed and submitted to Federal Student Aid, an office under the Department of Education.

Private student loans are in accordance with the benchmark levels of the US Federal Reserve and the London Interbank Offered Rate (LIBOR). Legislators rely on the latest market developments and 10-year Treasury which also adds pressure to lending rates. The Ratification of the Success of Real Opportunities and Prosperity through the Education Reform Act or PROSPER also affects student loans. The Ratification of the Success of Real Opportunities and Prosperity through the Education Reform Act or PROSPER also affects student loans. There is a good chance for this Statute to be approved because it includes the highly anticipated amendments to the Higher Education Act of 1965. The PROSPER Act seeks to support American students and enables them to complete low-cost post-secondary education in preparation for future employment.

See also

- Student financial assistance in the United States

- Tuition in the United States

- EdFund

- Free education

- Higher Education Bubble

- Higher Education Price Index

- Post-secondary education

- Private universities

- Student benefits

- Education Bureau

- Learning center

- Student debt

- student loans

- Tuition

- Freeze tuition

- Institute of Higher Education Access and Success

References

#9 (PNC ...")

Further reading

- Loonin, Deanne. Student loan law: Collections, intercepts, delays, disposals, repayment plans, and violations of trading schools. Boston: National Consumer Law Center, 30 June 2006. ISBN: 978-1-60248-001-8

- Student loan program: Travel through the world of education, collection, and litigation loans. Mechanicsburg, Pennsylvania Pennsylvania Bar Institute, c2003. vii, 300 p.Ã,: forms; 28 cm. ASIN B000IB82QA

- Wear Simmons, Charlene. Student Loans for Higher Education . Sacramento, California: California Research Bureau, State Library of California, 2008. 59 pages. ISBNÃ, 1-58703-233-3

External links

- "College, Inc.", PBS documentary FRONTLINE, May 4, 2010

- US. Department of Education

Source of the article : Wikipedia